Darmowa dostawa dla zamówień powyżej 299,00 zł.

Zostań członkiem wspólnoty miłośników książek z całego świata i zyskaj mnóstwo korzyści.

Załóż konto bezpłatnie

Darmowa dostawa z usługą Inpost oraz Orlen od 299.00 zł

DPD Kurier 12.99 zł

Poczta Polska 18.99 zł

Paczkomat 13.99 zł

InPost 12.99 zł

Punkt DPD 13.99 zł

Kontakt

Kontakt Jak kupować

Jak kupować

Pomoc

Dostawa

DPD Kurier 12.99 zł

Poczta Polska 18.99 zł

Paczkomat 13.99 zł

InPost 12.99 zł

Punkt DPD 13.99 zł

Darmowa dostawa z usługą Inpost oraz Orlen od 299.00 zł

Doradca ds. zakupów

Jesteśmy tu dla Ciebie!

(32) 444 93 66

Moje konto

▸

Pusty :-(

0

Darmowa dostawa dla zamówień powyżej 299,00 zł.

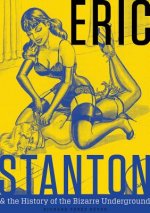

Basel II Risk Parameters

Estimation, Validation, Stress Testing - with Applications to Loan Risk Management

Język

Angielski

Angielski

Angielski

Książka

Twarda

The estimation and validation of the Basel II risk parameters PD (default probability), LGD (loss gi...

Cały opis

Kod Libristo: 01656741

?

268 b

268 b

268 b

470.87

zł

Dostępna u dostawcy

Wysyłamy za 10-13 dni

Nawet do 30 dni na zwrot

Klienci kupili także

/

/

binding.

binding.

281.01

zł

281.01

zł

The estimation and validation of the Basel II risk parameters PD (default probability), LGD (loss given default), and EAD (exposure at default) is an important problem in banking practice. These parameters are used on the one hand as inputs to credit portfolio models, on the other to compute regulatory capital according to the new Basel rules. The book covers the state-of-the-art in designing and validating rating systems and default probability estimations. Furthermore, it presents techniques to estimate LGD and EAD. A chapter on stress testing of the Basel II risk parameters concludes the monograph.

Aktorka

&

Poliglotka

EWA KASP

dla

Odtworzyć wideo

Libristo ma największy wybór literatury obcojęzycznej. Dlatego tutaj kupuję swoje książki.

Informacje o książce

Pełna nazwa

Basel II Risk Parameters

Autor

Bernd Engelmann, Robert Rauhmeier

Język

Angielski

Angielski

Oprawa

Książka - Twarda

Data wydania

2011

Liczba stron

426

EAN

9783642161131

ISBN

3642161138

Kod Libristo

01656741

Waga

750

Wymiary

158 x 241 x 29

Podaruj tę książkę jeszcze dziś

To łatwe

1 Dodaj książkę do koszyka i wybierz „dostarczyć jako prezent” 2 W odpowiedzi wyślemy Ci bon 3 Książka dotrze na adres obdarowanegoMogłoby Cię także zainteresować

/

Miękka

76.96

zł

/

Miękka

76.96

zł

/

Miękka

63.88

zł

/

Miękka

63.88

zł

Doradca książkowy Libroamiko

Korzystając z czatu, komunikujesz się z generatywną sztuczną inteligencją. Tym samym wyrażasz zgodę na przetwarzanie danych osobowych.

Cześć! Jestem Libroamiko, Twój doradca książkowy.

Jak mogę Ci pomóc?

Cześć, jestem Libroamiko, w czym mogę pomóc?